That’s because when a firm’s coffers are running low, when cash flow is an issue, and working capital remains a lifeline — i.e., the need for credit looms — the would-be borrower looks like a poor credit risk.

There’s evidence that for small businesses and the regional banks on which they rely, the spigot is being turned, if not to the “off” position, then to a point where funding has slowed to a trickle.

The pressure’s been apparent in the new age of inflation, even before the bank runs that marked the first quarter of this year. As noted by the Federal Financial Institutions Examination Council (FFIEC), in 2021 versus 2020, the dollar amount of small business loans originated decreased by 21%, to about $371 billion. The Kansas City Fed noted in its own data that year over year, small business loans declined by 17.7%.

And more recently, as noted here, the current friction on Capitol Hill regarding the debt ceiling shows that 9% of small and midsized businesses (SMBs) report more problems securing their last loan than in previous attempts, per Bloomberg.

Online Merchants Have It a Bit Easier

Those are aggregate numbers, but if we start to get more granular, there may be a bifurcation taking shape. For the smaller businesses that operate through online channels, there are digital avenues and platforms geared towards eCommerce (and omnichannel commerce) that have been tapping into less traditional means of financing.

Consider, as one example, Amazon’s recent small business update, which disclosed that in 2022, the eCommerce giant and its third-party lending partners lent $2.1 billion to independent sellers, which represents a 50% increase over the previous year. Elsewhere, during earnings season, Shopify said it had extended $477 million in merchant advances and loans in the first quarter of the year. Fourth quarter activity showed that merchants got $324 million in loans, up 21% year over year.

But the question looms as to what happens with the other Main Street SMBs, the ones that might be seasonal in nature, the ones that are perhaps more readily pressured by macro forces.

The overall small business lending pullback, as described above, may not bode well for Main Street SMBs.

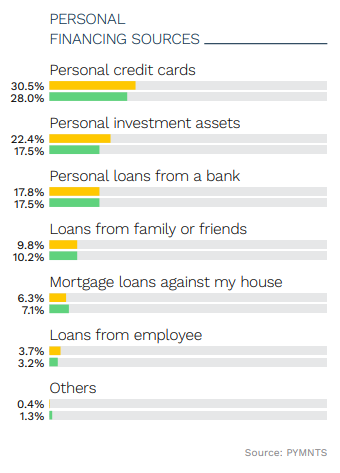

As detailed in the latest quarterly study on Main Street SMB health, the cash situation is indeed crunched, as only about a quarter of firms surveyed said that they have access to more than 60 days of cash. As many as 17% of firms have access to no cash cushion whatsoever.

Fully half of construction firms say they have access to less than 30 days’ worth of cash; about 45% of hospitality firms say the same. These businesses depend on large-ticket spending from end consumers, and are seasonal — and are certainly brick-and-mortar, which means that operating costs are high too.

As to where they’re getting the funds? PYMNTS data reveal that roughly a third of them are tapping into personal credit cards — only about 17% are getting funding from banks.