Rewriting Definitions For A Digitizing Landscape

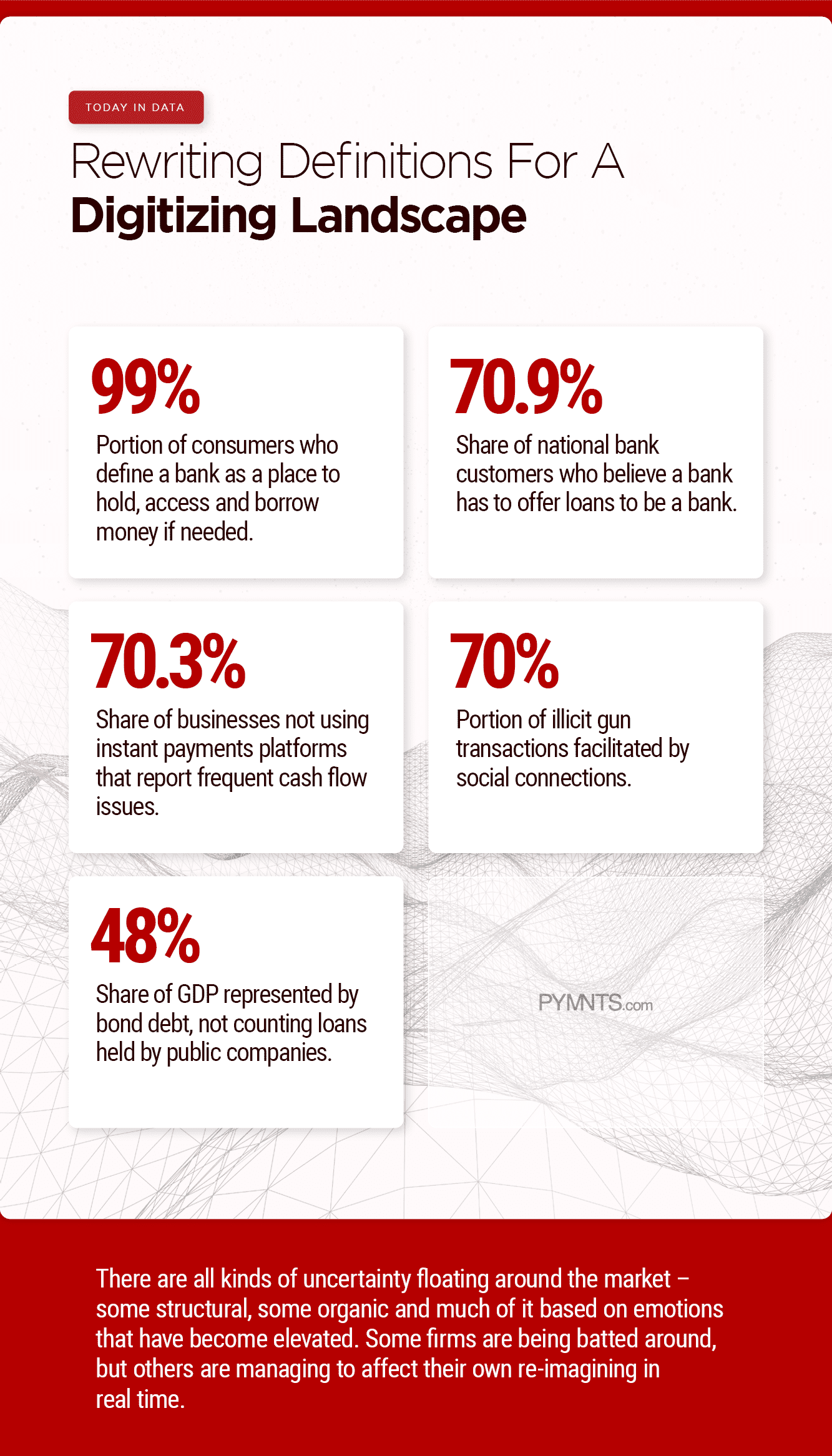

There is no shortage of questions that seem basic, but are harder to answer than they appear on first glance. What counts as a bank? When will instant payments be truly accessible, as opposed to only partially so? How can we track illegal transactions between people who know each other, and can easily and anonymously move money among themselves? And what to do with a giant pile of corporate debt – particularly as the public markets are getting bumpy? Okay, maybe that last one doesn’t look so basic from the outside. But they’re all hard to answer – and the need to find those answers is becoming increasingly pressing.

Data:

Data: