According to a PYMNTS Intelligence report, “Financially Struggling Consumers Are Twice as Likely to Face Payment Declines,” while payment declines have decreased overall, consumers living paycheck-to-paycheck remain more vulnerable. These consumers encounter payment failures at much higher rates, particularly when making essential purchases. This issue is intensified by the rising frequency of debit card rejections, which now outpace credit card failures by a large margin.

Struggling Consumers Face Higher Decline Rates

Between September 2022 and September 2024, payment declines across the consumer population fell from 18% to 12%. This reduction is attributed to advances in fraud detection and payment technology. But financially struggling consumers still report high rates of payment failures, with 23% experiencing at least one decline in the prior month — nearly double the national average.

This group is nearly four times more likely to face payment declines compared to those not living paycheck to paycheck. Among consumers who do not struggle with bill payments, just 6.3% encountered payment failures, compared to 23% among those facing financial strain. Even those who manage to make ends meet month-to-month are more likely to experience declines than their financially stable peers, though at a considerably lower rate of 9.1%.

Declines on Essentials Create Greater Strain

Payment declines are especially disruptive when they occur during essential purchases, such as groceries. Among struggling consumers, 7.1% of grocery transactions were declined, a rate 12 times higher than that of consumers not living paycheck to paycheck. Although this figure has improved, it has worsened since the spring of 2024, when only 3.3% of grocery payments were declined.

Retail payments are even more likely to be declined. Among paycheck-to-paycheck consumers struggling with bills, 8.1% of retail transactions were rejected, significantly higher than the 2.1% experienced by those who can comfortably pay their bills. In comparison, only 1.9% of retail transactions for financially stable consumers were declined.

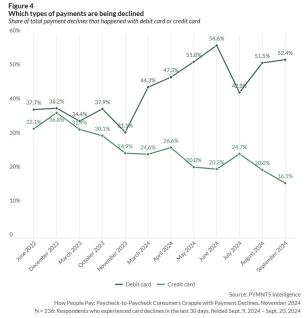

Debit Card Declines Surpass Credit Cards

Debit card transactions are now more than three times as likely to be declined compared to credit cards. In the past two years, the share of payment declines involving debit cards has risen by 40%, while the share involving credit cards has fallen by half, dropping from 32% to 16% in the same period. This trend underscores the challenges associated with debit cards, where declines are often unavoidable if account balances are insufficient.

The drop in credit card declines can be linked to accelerated access to financial tools such as mobile banking apps, which allow consumers to monitor their accounts and manage payments more effectively. Meanwhile, the rise in debit card declines reflects the direct impact of insufficient funds in checking accounts.

The increase in debit card declines and decrease in credit card rejections highlight the financial pressures facing consumers today. As debit cards remain a primary payment method for daily transactions, many people are experiencing payment failures due to insufficient funds, adding to the financial strain for those already struggling.