Consumers both want and need to engage with their financial institutions (FIs) digitally, but they want these interactions to be highly personalized.

Branch closures rendered digital banking a necessity, and now it is a permanent fixture of the business landscape.

Banks closed 9% of their branches in 2021. While these moves were in response to pandemic-era decreases in customer demand for in-person banking, this shift has created a new need for digital services to take the place of amenities previously accessed via a branch. A recent Citizens Financial Group survey found that most consumers now do at least some of their banking digitally, and more than 70% view their digital shifts as permanent.

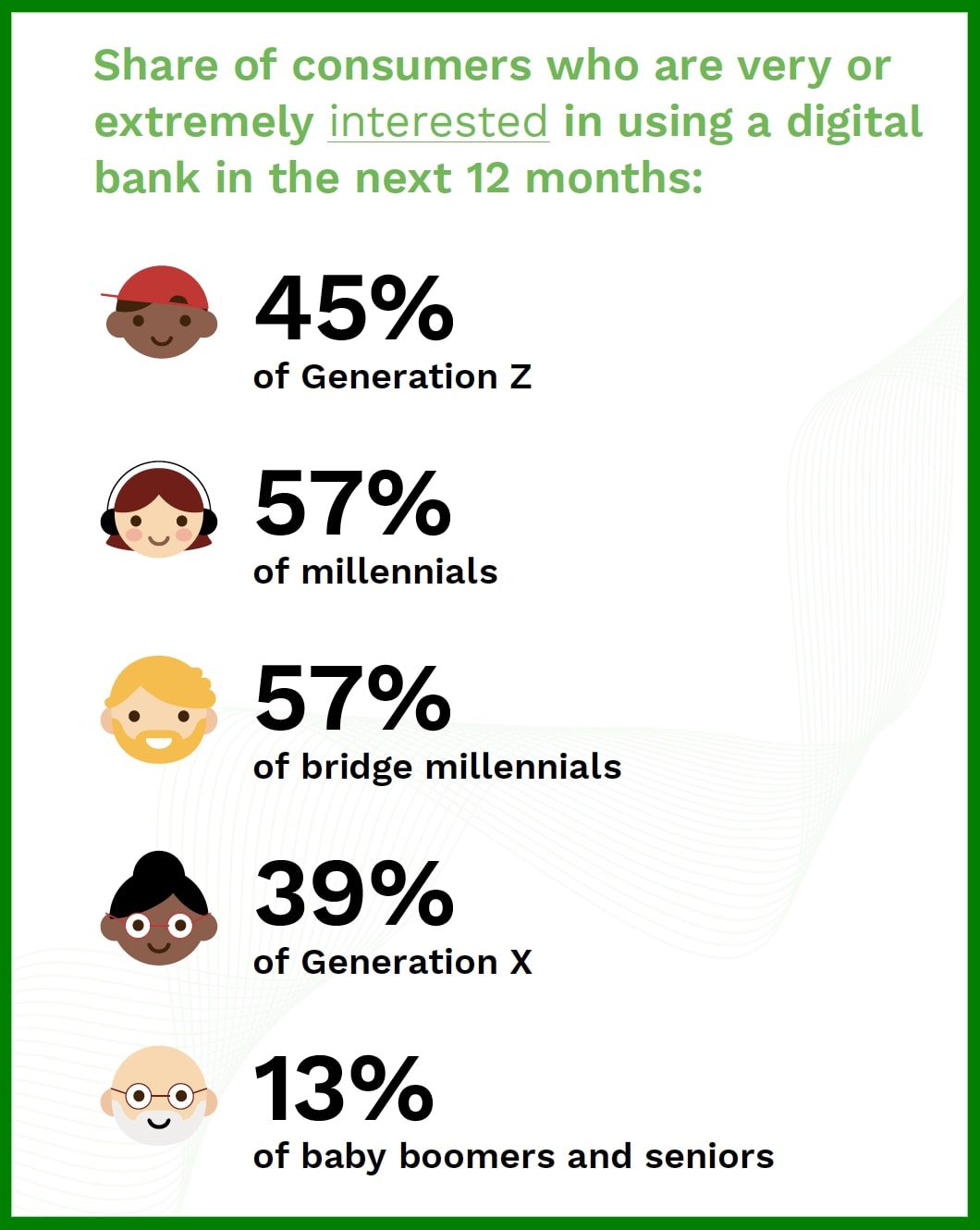

Most consumers are at least curious about digital banking.

Fifty-nine percent of consumers say they are at least somewhat interested in trying digital banking over the coming 12 months, and 36% say they are very or extremely interested in this. The most common motivation is faster and easier transfers followed by lower costs and fewer fees. Younger generations are leading the pack.

Consumers are highly willing to use digital banking, but they may not be fully won over yet.

More than 70% of banking customers in every geographic region and age demographic are willing to consider digital channels. An equal share — 70% — of customer service interactions now occur on mobile, nearly twice as many as in 2017. Despite this apparent endorsement, mobile service use was nearly 10 percentage points higher than customer preference in 2021, indicating that banks still have work to do in fully converting customers to digital and mobile services.

A yearning for more personalized banking experiences is widespread, especially among younger consumers

A survey of 3,000 global consumers found that banking customers are seeking more personalized mobile experiences that offer full service anytime, anywhere.  More than 80% of Gen Z consumers surveyed want to be able to take care of even complicated tasks using digital channels, such as completing loan applications or adding personal. details to a profile to obtain tailored product recommendations. Ninety-eight percent of consumers surveyed also want fast answers to their banking questions, yet 58% say their FIs have granted them this experience.

More than 80% of Gen Z consumers surveyed want to be able to take care of even complicated tasks using digital channels, such as completing loan applications or adding personal. details to a profile to obtain tailored product recommendations. Ninety-eight percent of consumers surveyed also want fast answers to their banking questions, yet 58% say their FIs have granted them this experience.

A positive technology experience leads to consumer trust — but sometimes human interaction is needed.

Banks that are unable to provide their customers with good experiences are unlikely to have customers say they trust them. Banks can also promote a trusting relationship with their clients by knowing when to move from a digital interaction to a human one. When an issue is not immediately resolved, 41% of consumers surveyed say they want to be able to switch from a chatbot to a customer service representative from inside the messaging application.

While digital banking’s convenience is here to stay, the human touch will remain essential to an excellent customer experience.

While there is no going back to the pre-digital era, the ability to interact with other humans, whether in person or through a virtual channel, is still a core necessity for most bank customers, especially when accessing financial advice and working through complex transactions. Two-thirds of both consumers and businesses prefer human interaction and know-how when receiving any kind of financial advice. Combining the human touch and a positive technology experience is how digital FIs can retain customers in this highly competitive environment.