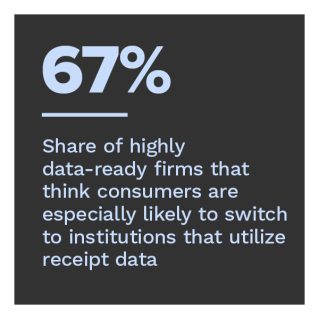

Leveraging the full value of item-level receipt data in a simple, secure way enables financial institutions (FIs), FinTechs and merchants to provide the rich, seamless commerce and banking experiences today’s digitally savvy consumers expect. For firms looking to integrate item-level receipt data, the potential to attract new customers is a key driver. Seventy-two percent of companies surveyed believe consumers would switch to firms that provide solutions based on the use of receipt data.

No matter their level of data readiness, our research has found that firms face implementation issues when integrating item-level receipt data into their operations, especially when it comes to supporting their customers and enabling merchant innovation. The leading issue firms face is integration with existing card-linked offer programs, with nearly half of financial service providers reporting this as the most difficult challenge. Firms must also implement certain measures to use receipt data to its full potential, and data security and standardization are among these leading requirements.

“Meeting the Need for Item-Level Receipt Data: How Integration Enables Innovation,” a PYMNTS and Banyan collaboration, examines the implementation issues FIs and FinTechs face when integrating item-level receipt data into their operations. We surveyed 351 executives representing FIs with at least $5 billion in assets and FinTechs with at least 1 million active monthly users between June 30 and July 27, to explore how this integration can help merchants track customer spending, provide loyalty and rewards programs and enable innovative uses of item-level receipt data.

More key findings from the study include the following:

More key findings from the study include the following:

• To use receipt data, firms must implement data-related capabilities. While 46% of firms consider data standardization necessary to enable the use of item-level receipt data, 45% consider data privacy or security essential. This share is higher for firms with high data readiness, with 51% of these businesses considering data standardization necessary to using receipt data. Newer data processing technologies, such as machine learning (ML) or artificial intelligence (AI), are regarded as necessary by just 22% of firms, yet FinTechs and high data-readiness firms are more likely to consider these technologies necessary.

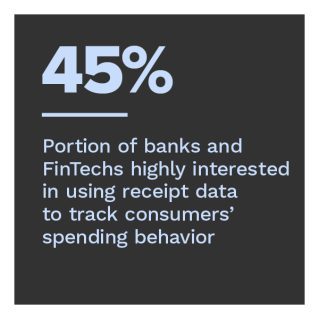

• Data standardization is particularly important for firms using item-level receipt data to track consumer spending behavior, and more than half of these firms consider this capability necessary. Among firms using item-level receipt data to track consumer spending behavior, 53% consider data standardization a necessary capability.  This allows firms to understand consumer spend patterns and trends in a meaningful, consistent way. Fifty-one percent of firms using receipt data for loyalty and shopping offers consider this capability important, while 48% of that group consider data privacy or security a necessary feature. A smaller share of firms that use item-level data for fraud solutions — 43% — consider data privacy or security essential. Additionally, 30% of firms using receipt data for streamlining expense management consider ML or AI essential.

This allows firms to understand consumer spend patterns and trends in a meaningful, consistent way. Fifty-one percent of firms using receipt data for loyalty and shopping offers consider this capability important, while 48% of that group consider data privacy or security a necessary feature. A smaller share of firms that use item-level data for fraud solutions — 43% — consider data privacy or security essential. Additionally, 30% of firms using receipt data for streamlining expense management consider ML or AI essential.

• Improving data-related capabilities can help firms struggling to integrate receipt data into their existing loyalty and card-linked offers or those experiencing difficulties building new digital receipt functionalities to engage merchants and consumers. Approximately half of these firms believe data privacy or security and data standardization are essential to using item-level receipt data. Forty-eight percent of firms that consider card-linked offer programs to be the most difficult area for receipt data integration believe data privacy or security is essential to using receipt data, while 42% think data standardization is essential.

To learn more about how banks and FinTechs are addressing key implementation issues when integrating item-level receipt data into their operations, download the report.