In a climate of economic uncertainty and consumer dissatisfaction, it is crucial that insurance companies understand what customers are looking for from their insurance providers. Companies that fail to meet consumers’ needs risk losing out to those that do — and competition is increasingly fierce.

The funding of InsurTechs — startup companies taking a technology-first approach to insurance — is growing, for example. According to one report, InsurTech investment more than doubled between 2019 and 2021, up from $7.2 billion to $14.6 billion worldwide. The same report noted that InsurTechs are committed to improving consumer satisfaction by leveraging a digitally enhanced customer experience. It appears these efforts are working, moreover, with a survey finding that InsurTechs outperformed traditional insurance companies when it came to speed and visual appeal to consumers.

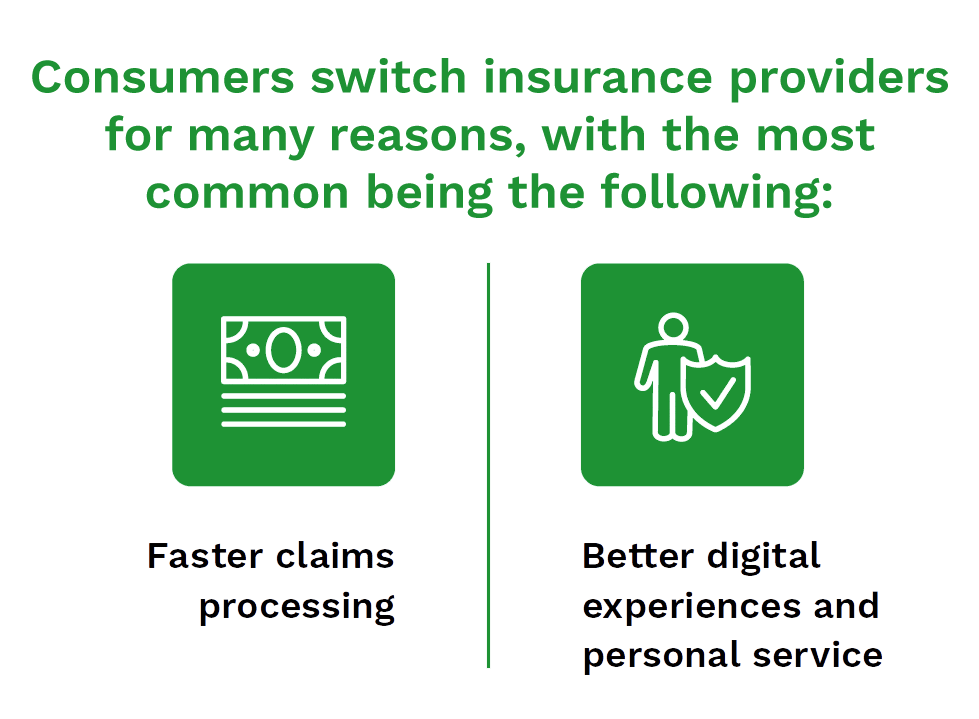

Consumers want faster payments and an easier claims process.

Heavy competition makes it more important for insurance companies to gauge their customers’ preferences. Near the top of these preferences is speed. A survey of U.S. and Canadian policyholders found that more than half of respondents who had switched insurance providers in the last year indicated they did so for faster claims processing. The survey found that in the auto insurance space, the biggest frustration when filing claims was a delay in payouts.

The same survey found that other top reasons for switching included an interest in better digital experiences. As another report noted, consumers have come to expect insurance companies to offer the same digital-first experiences they are accustomed to enjoying with tech companies. The use of digital shopping tools to help users find discounts, policy details and unique coverage options leads to better customer satisfaction results.

Consumers are also interested in contextual insurance offers. A PYMNTS survey found that 45% of consumers were at least very interested in their FIs using transaction history to present insurance coverage options. Unsurprisingly, consumers who used digital banks were more likely to favor such digital offerings, with 70% of this consumer type at least very interested.

Digitization and payment speed must be balanced with fraud risk.

While it is important for insurance companies to pursue innovation related to payment speed and digital offerings, they must be mindful of fraud. Fraud is a considerable — and growing — concern in the insurance industry. In 2020, for example, insurance professionals suspected that 18% of claims were fraudulent, but by 2022, this figure rose to 20%. The problem is that by accelerating the insurance claim and payments process, companies risk increasing the potential for fraud if these innovations are not done correctly.

This is why fraud prevention measures are essential to companies’ digital innovations. One PYMNTS study, for example, found that 94% of finance and insurance companies rolled out fraud detection systems when digitizing their payments processes — well above the rate of companies in other industries taking similar measures.