Neobanks, nonbanks, and a host of other constructs fall under the heading “FinTech,” and while broadly popular with the digital-first economy, specific user profiles emerge on closer examination.

PYMNTS analyzed this in “The Disbursements Satisfaction 2022: The Role of FinTechs,” a collaboration with Ingo Money, and part of The Disbursements Satisfaction 2022 series.

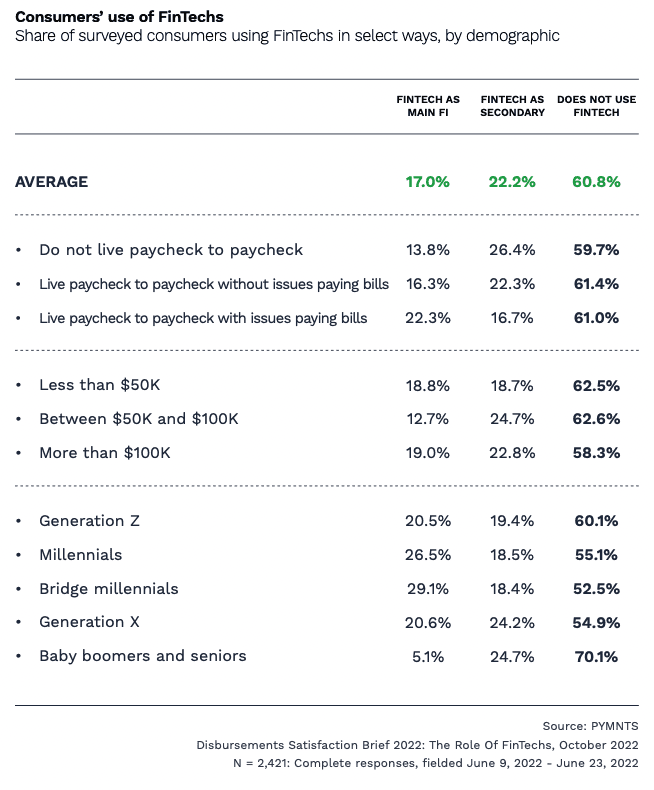

In a survey of over 3,600 United States consumers, we found that 39% use FinTechs in some capacity, whether as their primary or secondary financial institution (FI). This indicates that at least 68 million U.S. consumers use FinTechs to some extent, often to receive or send money in peer-to-peer (P2P) fashion.

However, the study stated that “FinTechs are especially popular among low-income consumers who live paycheck to paycheck with issues paying bills,” with 39% of consumers in that bracket using FinTechs and 22% using them as their primary FI.

Among consumers who do not live paycheck to paycheck, only 14% use FinTechs as their primary FI.

“They are more likely to use FinTechs as secondary FIs, with 26% doing so,” the study found.

While similar trends are observed among high-income and low-income consumers, large numbers of both types of consumers are using FinTechs.

“The difference is that high-income consumers are more likely to use FinTechs as secondary FIs than primary FIs, while low-income consumers use them as primary and secondary FIs in roughly equal measures,” per the study.

These stats lead to the conclusion “that although consumers of a wide variety of financial backgrounds use FinTechs, those who use them as primary banks may see them as cost-effective alternatives to traditional banks and credit unions.”

Additionally, we found that “consumers who use FinTechs as their primary FI also tend to use them for a wider mix of what might be considered ‘quotidian’ financial products, including ATMs, credit cards and debit cards, compared to consumers who use FinTechs as secondary FIs.”

Among consumers who use FinTechs as secondary FIs, P2P payments are the predominant use case.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More