As instant payments become the norm, businesses can bolster safeguarding their hard-earned revenue.

While legacy habits such as paper checks persist, small businesses are catching up with their larger competitors in modernizing their finance systems. Swapping traditional methods for efficient alternatives such as real-time payments is increasingly the norm, as 41% of all U.S. businesses use some form of instant payments. This adoption rate is set toward continued growth given real-time payments’ ease and speed compared to bulkier predecessors.

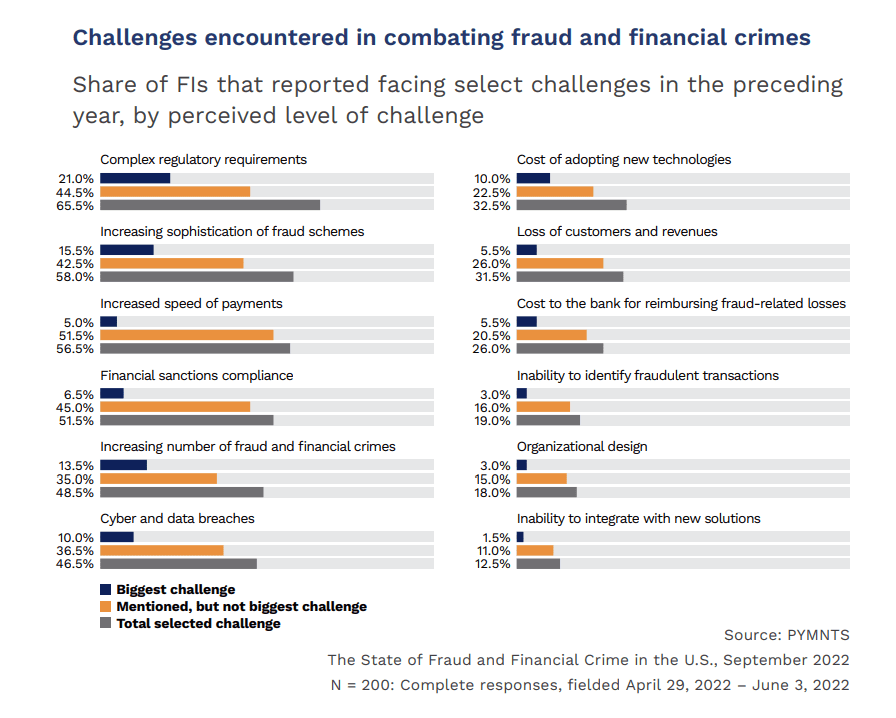

However, these conveniences could come at the price of a whole new set of schemes perpetrated by hackers and other bad actors. As the transaction’s speed could make detection more difficult in manual reconciliations, some businesses may consider implementing increased fraud-fighting capabilities. As noted in the February “B2B Payments Fraud Tracker®,” a PYMNTS collaboration with nsKnox, financial institutions (FIs) partnering with businesses recognize the potential for fraud and associated crime that comes along with the increased speed of payments.

The issues encountered by FIs fighting fraud in their real-time payments capabilities is top-of-mind for these institutions, as fraud costs the sector a collective $51 billion per year. When surveyed, 57% said it was a challenge for them in the previous year. While bank and other FIs’ fraud tools are effective, businesses can bolster these safeguards to decrease the chances of their funds falling prey to hackers and other bad actors.

In an interview with PYMNTS, Nithai Barzam, chief operating officer of FinTech security firm nsKnox, detailed the importance of firms implementing capabilities in partnership with those used by their banks. “So many [businesses] talk about faster, real-time, immediate payments,” he said. “This is great to be able to pay and receive money quickly, but it also opens the door for what’s known as ‘faster fraud’ and closes the window of time to confirm compliance with anti-money laundering and anti-terror financing regulations.”

While larger firms may create some of these technologies in-house, smaller businesses may not have the same resources. Their efforts could be better suited to finding a third-party solution to either implement themselves or outsource entirely; 31% of businesses plan to outsource their identity checks.

Different partners excel at different solutions for protecting their business clients from fraud. Card-issuing platform Marqeta’s suite is designed to provide Marqeta’s customers with risk, compliance, and fraud management capabilities across its cardholders’ lifecycle. Also targeted toward retailers and merchants, machine learning platform Ravelin has joined with Mastercard to integrate enhanced digital identity verification capabilities to secure quick commerce. Using partner technology, Ravelin will verify digital identities and analyze real-time fraud insights to streamline the validation of a consumer’s identity without added friction.

For the broader business payments landscape, Galileo’s Payment Risk Platform targets B2B card transactions through the payment ecosystem. It combines fraud analytics with AI technologies to enhance its end-to-end risk management platform, including support for debit and credit transactions, ACH, and provisioning against payment fraud.

While relying on their FI’s fraud innovations is a choice, it may not be the most secure decision for small businesses considering implementing innovations such as real-time payments. A few safeguards put in place to work in conjunction with the bank’s tools may well pay for themselves in saving lost revenue and unnecessary headaches.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More