Credit unions (CUs) have delayed their entry into the market for cryptocurrency products and services, largely because financial regulations bar CUs from holding digital assets on their balance sheets. At the same time, many credit union executives say they do not fully understand digital currencies — and they do not believe their members have much of an understanding, either.  Eighty percent of the executives we surveyed have little to no interest in offering crypto products and services.

Eighty percent of the executives we surveyed have little to no interest in offering crypto products and services.

But rivals are not waiting around for credit unions to warm up to the idea of offering crypto options. CU executives may have no choice but to overcome their reluctance or else risk being disintermediated by the crypto exchanges, FinTechs and other financial institutions that are willing to offer cryptocurrency products and services.

In “Credit Union Innovation: Cryptocurrency as a Key to Member Loyalty,” a PYMNTS and PSCU collaboration, we surveyed 6,483 consumers, 101 credit union executives and 51 FinTech executives. We examined the level of interest members have in innovative digital financial offerings, including crypto payment products, as well as credit unions’ efforts to satisfy this growing demand.

22%: The share of credit union executives who are interested in providing cryptocurrency services to members.

Of the credit union executives who say they are interested in making cryptocurrency products and services available, none actually offer these products. FinTechs are in a much more advanced position — 22% already offer crypto products, and another 22% have at least some interest in doing so. The disparity between how CUs and FinTechs approach crypto products underscores how innovative and aggressive competitors have set themselves apart from more cautious financial organizations.

Of the credit union executives who say they are interested in making cryptocurrency products and services available, none actually offer these products. FinTechs are in a much more advanced position — 22% already offer crypto products, and another 22% have at least some interest in doing so. The disparity between how CUs and FinTechs approach crypto products underscores how innovative and aggressive competitors have set themselves apart from more cautious financial organizations.

29%: The proportion of consumers who say they value product innovation enough to leave their primary financial institution for another bank or credit union.

The share of consumers who have such a strong interest in product innovation is a five-percentage-point increase from the 24% who said the same thing in 2021. Another 47% of financial institution account holders say product innovation is important to them, although they would likely not switch where they keep their accounts to pursue it.

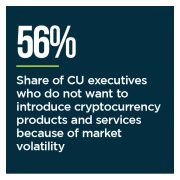

51%: The portion of credit union executives who are reluctant to offer cryptocurrency products to members because they do not understand crypto.

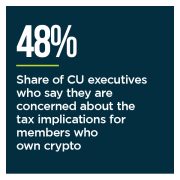

Credit union executives’ reluctance to enter the crypto market stems from the obstacles they must overcome before a substantial portion of their members are set up to trade or pay with crypto. Executives are also concerned about crypto’s tax implications and the lack of a sufficient number of merchants who are willing to accept crypto payments.

CUs need to assess the benefits of rolling out crypto products and the risks of failing to offer the cryptocurrency products and services that appeal to customers.

To learn more about how credit unions can capitalize on their members’ growing demand for cryptocurrency products, download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More