Financial institutions (FIs) face tough decisions when trying to keep their clients safe. Customers and merchants rely on their banks and credit unions (CUs) to ensure they have secure, convenient online transactions, and many FIs work to detect fraud by looking for abnormal purchasing behaviors that could indicate something is amiss.

Seeing consumers’ cards suddenly used in new cities or for making unusual types of purchases could be a major red flag that indicates the cards have been stolen, for example. But FIs are being met with the new challenge of shifting consumer behaviors as they weather stay-at-home mandates and primarily shopping online, potentially making unusual purchases because they are no longer able to visit brick-and-mortar stores. The FIs must decide in situations like these whether freezing the card payments will rescue the cardholders from fraudsters’ attacks or block legitimate customers from getting the items they need.

The inaugural FI Fraud Decisioning Playbook explores how banks and CUs can better make these kinds of high-stakes determinations, such as by drawing on the digital transaction histories their customers have across a variety of platforms and using artificial intelligence (AI)-powered tools to analyze this data in minute detail. These insights and tools equip FIs with deep understandings of legitimate customers’ behaviors and thus help them spot fraudsters while reducing the likelihood of false positives.

Around The FI Fraud Decisioning World

The coronavirus pandemic has sent more consumers purchasing online, and bad actors are launching more schemes intended to swindle honest shoppers out of their money. Banks must stay ahead of the criminals and are redesigning their fraud decisioning approaches to more quickly detect account takeovers without accidentally flagging genuine customers as fraudsters.

Consumers’ shift to digital banking and purchasing while living under stay-at-home orders has meant that banks must be especially vigilant against online and mobile fraud. Criminals are particularly targeting mobile channels, but FIs can prepare strong defenses by pooling different data sources to create more detailed, comprehensive pictures of normal customer behavior. FIs armed with solid understandings of legitimate activity will thus be able to more quickly detect abnormalities that indicate fraudsters at work.

AI is vital in helping banks analyze such data pools and defend themselves against attacks like loan application fraud. Bad actors are increasingly using synthetic IDs to win loan approvals and then make off with the money with no intention of repaying. AI-powered tools can help lenders catch irregularities that humans might miss, however, which enables the FIs to block out the criminals and direct loans to those who actually need them.

AI is vital in helping banks analyze such data pools and defend themselves against attacks like loan application fraud. Bad actors are increasingly using synthetic IDs to win loan approvals and then make off with the money with no intention of repaying. AI-powered tools can help lenders catch irregularities that humans might miss, however, which enables the FIs to block out the criminals and direct loans to those who actually need them.

To find more about these and the rest of the latest headlines, download the Playbook.

AI-Powered Analysis Of Transaction Data Fuels Fraud Fighting

FIs need to have accurate, informative understandings of what normal, fraud-free transactions look like for their merchant clients and those merchants’ customers. That will enable the FIs to better catch deviations that could indicate bad actors at work without confusing legitimate transactions for fraudulent ones, explained Wells Fargo Head of Merchant Services Colleen Taylor. In this month’s Feature Story, Taylor explains how banks can leverage their deep stores of transactional data to get the kinds of insights that help them rapidly detect fraud attempts. FIs’ fraud assessment systems must be flexible as well so that the systems can be updated to remain accurate even as events like the COVID-19 outbreak change what normal purchasing behavior looks like, she said.

Read the full story in the Playbook.

Read the full story in the Playbook.

Deep Dive: FIs And The Importance Of Customer Data

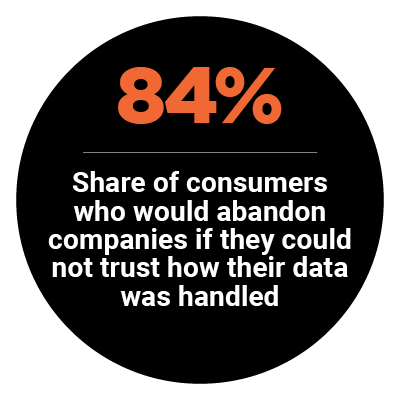

Gas station chain Wawa saw 30 million payments card details posted for sale online after a recent data breach. Criminals eagerly purchase personal data stolen from merchants and FIs in these kinds of breaches and use the information for perpetuating damaging fraud attacks. Banks must keep their customers’ personal information safe and thus need to find ways to access better data that can help them separate the fraudsters from the legitimate customers. This month’s Deep Dive examines how FIs are using innovative tools to safeguard data, including using AI and other automated technologies to help them quickly and accurately process details.

Get the scoop in the Playbook.

About The Playbook

The FI Fraud Decisioning Playbook, a PYMNTS and Simility collaboration, examines how understanding legitimate customers’ behaviors can help banks spot and eliminate malicious activities.