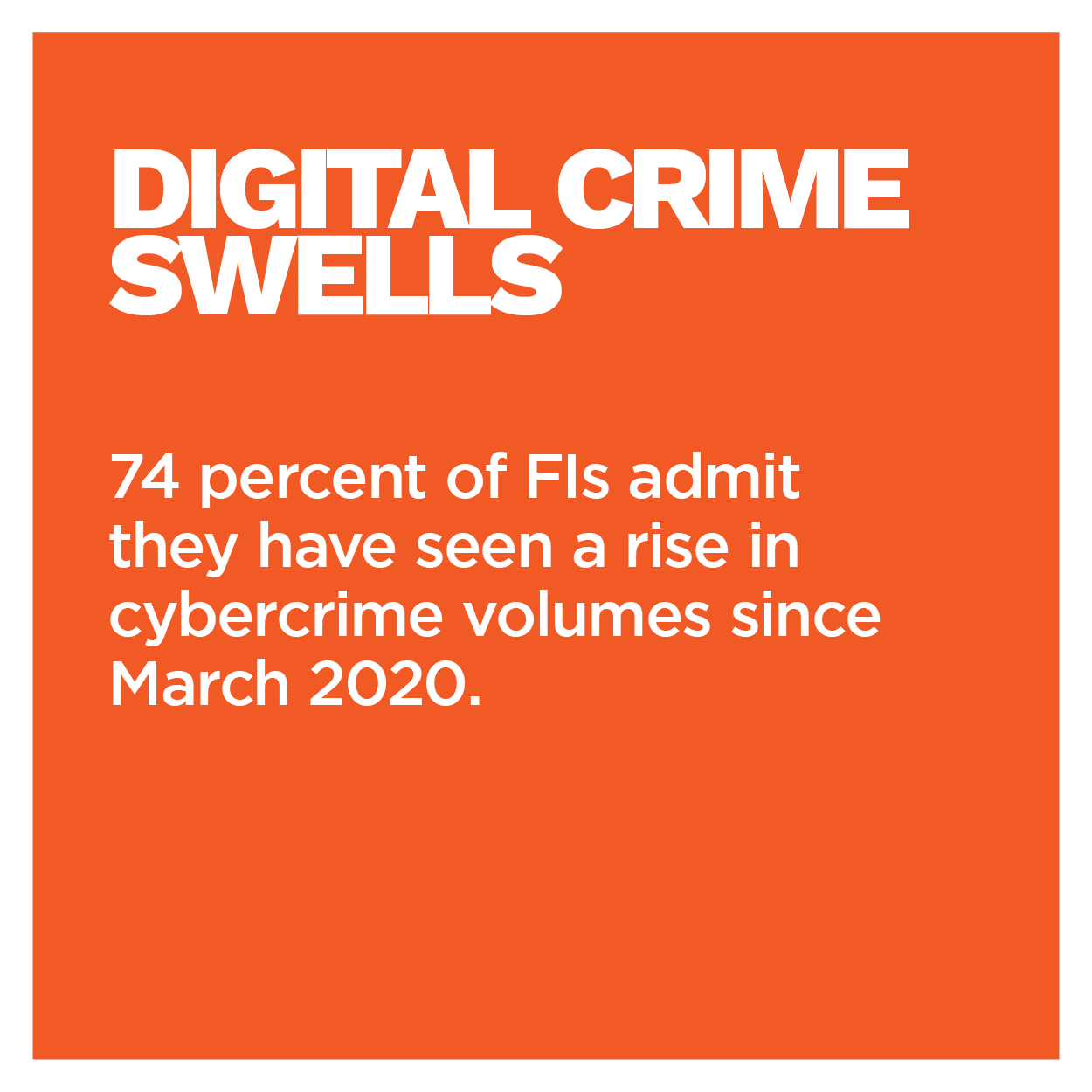

More businesses and consumers are conducting their daily tasks and transactions online, meaning offering seamless digital experiences is becoming increasingly important for today’s financial institutions (FIs). This also means banks must work to ensure their online services are kept secure against the bad actors as they follow customers’ lead, however. Seventy-four percent of banks claimed they have seen a rise in digital crime since March 2020, indicating they are well aware of the need for further protection.

Lawmakers are also paying close attention to t his increase, with many passing new regulations or updates to their existing anti-money laundering (AML) rules with the aim of clamping down on related fraud. This includes the Anti-Money Laundering Act of 2020 (AMLA 2020) recently passed by the United States Congress in January 2021, which aims to provide the country’s FIs with updated AML guidelines. It is therefore essential for businesses to ensure they are implementing AML solutions and tools that can keep out fraudsters while staying compliant with these new guidelines, without sacrificing the speed and convenience online banking users are expecting.

his increase, with many passing new regulations or updates to their existing anti-money laundering (AML) rules with the aim of clamping down on related fraud. This includes the Anti-Money Laundering Act of 2020 (AMLA 2020) recently passed by the United States Congress in January 2021, which aims to provide the country’s FIs with updated AML guidelines. It is therefore essential for businesses to ensure they are implementing AML solutions and tools that can keep out fraudsters while staying compliant with these new guidelines, without sacrificing the speed and convenience online banking users are expecting.

In the latest Preventing Financial Crimes Playbook: A Guide To Overcoming Commercial And Corporate Payment Fraud, PYMNTS analyzes why FIs must pay careful attention to emerging financial crime trends and why they must adopt enhanced AML and watchlist screening tools to isolate and oust cybercriminals.

Around The Payment Fraud Space

One space that is receiving increased attention from U.S. lawmakers in the face of growing fraud is the art world. Anonymous sales or unclear ownership records are common within this market, something that can attract criminals looking to use these factors to slip past AML or other financial restrictions. U.S. regulators are looking to see if they can apply existing laws such as the Bank Secrecy Act to art sales to cut down on the likelihood of money laundering or similar crimes. The Bank Secrecy Act requires FIs to supply lawmakers with documentation in the event of risky transactions over $10,000 in value, a standard that, if applied to the art market, could help to reduce the chances of fraud. The increased regulatory interest inside of this space makes it clear that lawmakers are paying close attention to current AML standards and sanctions as well as how they may need to change to keep pace with shifting fraud tactics.

Regulators in other markets are also updating their AML standards, including lawmakers in the European Union (EU). The market’s sixth version of its Anti-Money Laundering Directive (AMLD), 6AMLD, came into full effect on June 3, 2021. The latest iteration of the rule further expands the scope of the first directive passed in 1990 to hold new industries as well as company employees accountable for any violations. 6AMLD now covers eWallet and digital asset providers, and both such companies as well as their legal entities can be prosecuted for failing to comply with the regulation. Such companies as well as FIs within the EU must ensure they have security and AML solutions in place that fall within this rule’s standards.

Bad ac tors are continuing to attack online banks and businesses with the hopes of making off with stolen funds or personal information as such regulations take shape. Phishing attacks remain favorites among cybercriminals, for example, with one report finding phishing accounted for 33 percent of all fraud attempts that occurred in Q1 2021. This is an increase of 13 percent from the previous quarter. Such attacks can provide both short and long-term benefits for fraudsters, enabling them to access new data and funds immediately while also setting them up to conduct future fraud attacks or build out more robust synthetic identities with the stolen details. Protecting against them is therefore essential for FIs and businesses alike.

tors are continuing to attack online banks and businesses with the hopes of making off with stolen funds or personal information as such regulations take shape. Phishing attacks remain favorites among cybercriminals, for example, with one report finding phishing accounted for 33 percent of all fraud attempts that occurred in Q1 2021. This is an increase of 13 percent from the previous quarter. Such attacks can provide both short and long-term benefits for fraudsters, enabling them to access new data and funds immediately while also setting them up to conduct future fraud attacks or build out more robust synthetic identities with the stolen details. Protecting against them is therefore essential for FIs and businesses alike.

For more on these and other stories, visit the Playbooks News & Trends.

The FBI On Why FIs Must Adjust Their Financial Crime And AML Tactics To Ward Against Digital-First Fraud

More businesses and consumers are turning to digital channels first and foremost, and so are fraudsters. Cybercriminals are coming armed with an increasing variety of tools and technologies to skim money and personal data away from digital platforms, and many FIs may still lack the tools necessary to distinguish between legitimate customers and fraudsters. It is critically important for FIs to revamp their financial crime prevention strategies to respond to these shifts and to incorporate tools that allow them to make that distinction, a representative from the U.S. Federal Bureau of Investigation (FBI) told PYMNTS. To learn more about why FIs must revamp their financial crime protection strategies to respond to emerging fraud trends in a digital-first world, visit the Playbook’s Feature Story.

Deep Dive: How Innovative AML, Watchlist Screening Solutions Aid Compliance, Effectiveness In Fighting Digital-first Financial Crimes

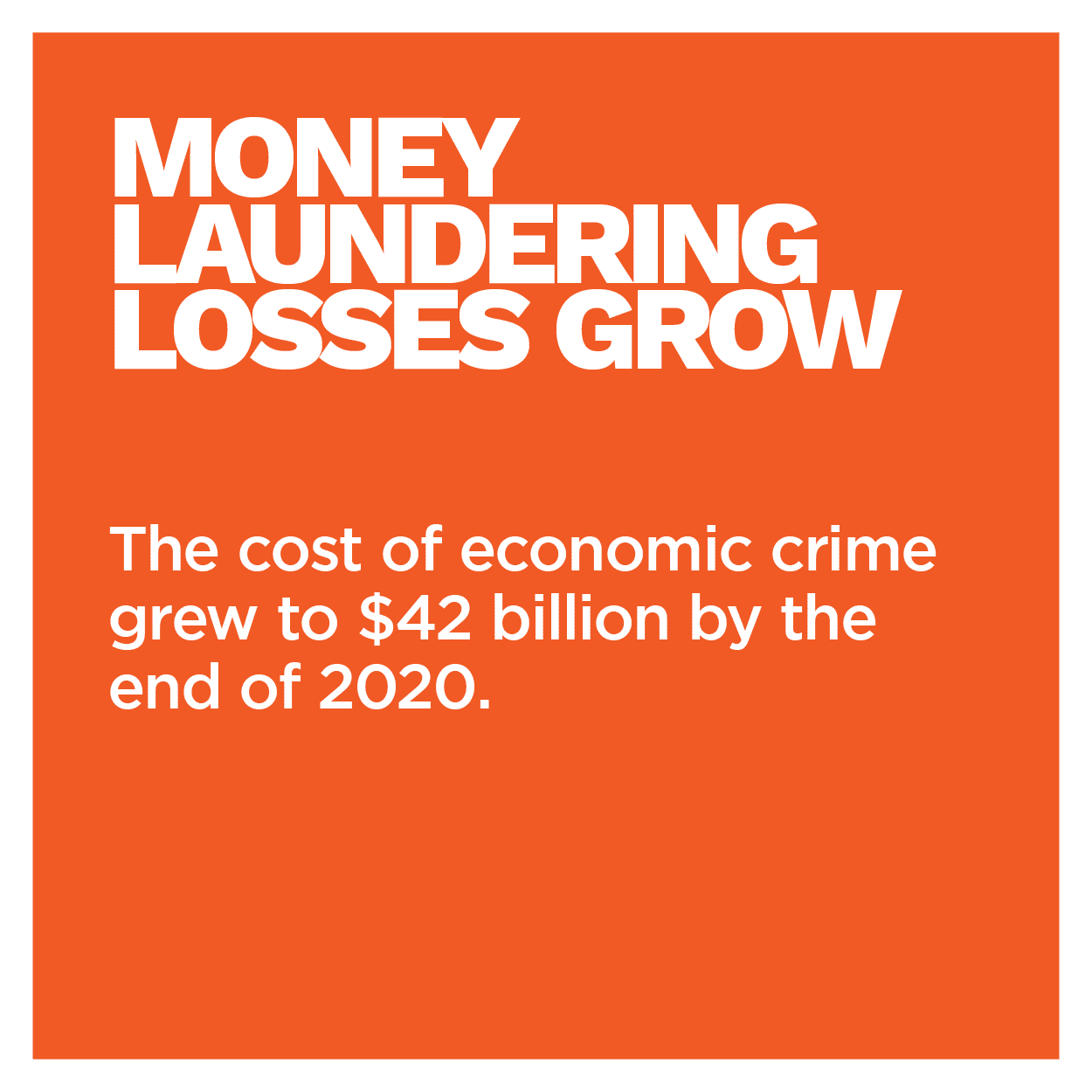

The events of the past year created yawning cybersecurity gaps that have yet to close, and bad actors are all too willing to take advantage of these weak points. Crimes such as money laundering are growing in both scale and cost for banks and businesses, for example, with one study finding the cost of money laundering globally has now reached $42 billion. This means banks must incorporate robust financial crime prevention solutions that can easily find and oust such bad actors without sacrificing the seamless user experience online-first consumers are now expecting. This is where enhanced AML and watchlist screening solutions could come into greater play. To learn more about how AML and watchlist screening solutions can help to protect against online financial crimes, visit the Playbook’s Deep Dive.

that have yet to close, and bad actors are all too willing to take advantage of these weak points. Crimes such as money laundering are growing in both scale and cost for banks and businesses, for example, with one study finding the cost of money laundering globally has now reached $42 billion. This means banks must incorporate robust financial crime prevention solutions that can easily find and oust such bad actors without sacrificing the seamless user experience online-first consumers are now expecting. This is where enhanced AML and watchlist screening solutions could come into greater play. To learn more about how AML and watchlist screening solutions can help to protect against online financial crimes, visit the Playbook’s Deep Dive.

About The Playbook

The Preventing Financial Crimes Playbook, a PYMNTS and Bottomline collaboration, examines how corporate and commercial payment fraud is evolving, which fraud risks are the most significant for businesses and which technologies and solutions can best safeguard their operations.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More