The “Modern Money Mobility Ecosystem,” detailed in a recent PYMNTS Intelligence benchmark report, is altering how money is accessed and moved through a network of banks, FinTechs and technology providers. This evolution makes accessing money faster and more efficient, while also enabling new ways for service providers to innovate financial services and strengthen customer relationships.

The ecosystem is characterized by an increasing number of players, layers, technologies and processes required to create the safe, secure, and seamless movement of funds in and out of accounts on demand and in real time. The report examines this intricate network, highlighting the key participants and the use cases propelling the demand for a more accessible and inclusive financial sector, driven by secular shifts such as instant P2P/Me2Me transfers, gig economy payouts, and corporate instant disbursements.

At its core, the money mobility ecosystem revolves around four elements: the payment; the account; the funding mechanics of money in, money out; and the processes for clearing, settlement and reconciliation.

Accounts serve as the central hub, acting as both the origin and destination for financial transactions and, significantly, presenting an opportunity to leverage a payment to establish a new account relationship. Competitive accounts are viewed as hubs of financial activity, needing to offer a wide array of services such as multiple payment options with instant funding, various use cases, and tools for management and integration.

A key development is the use of virtual accounts, which emerge as a tool to transform a payment from the sender’s account into a new one that can be monetized in different ways. This transformation allows corporates, often with the help of money mobility platforms and their treasury banks, to issue virtual accounts for purposes like instant tip disbursement or gaming winnings, turning an outbound payment into a foundation for a new closed-loop ecosystem offering incentives and monetization opportunities for account issuers.

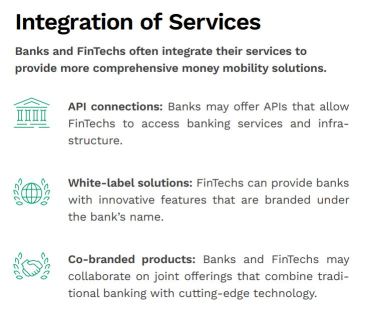

FinTechs also play a role here, facilitating money mobility for banks that may lack the infrastructure to easily issue and ledger new accounts.

Key data points from the report illustrate the scale and direction of this trend:

- U.S. consumers opened 200 million new accounts in the last 12 months, representing nearly one new account for 70% of all adults. Nearly half of new checking accounts were with FinTech platforms.

- Demand for instant payments is high: Over 80% of consumers opt for an instant payment if offered. Notably, 47% of small and mid-sized businesses (SMBs) are willing to pay a fee of 3.2% or a fixed fee of $14 per payment to receive a payment immediately.

- Adoption of instant payments by providers is rapidly increasing: The share of disbursement providers offering instant payments as a choice increased from 9.7% in February 2018 to 37% in July 2024, a 282% increase over six years.

The ecosystem’s complexity arises from this web of partnerships and integrations, notably the collaboration between traditional financial institutions and innovative FinTechs. Banks often serve a dual role, acting as primary account issuers leveraging established infrastructure and regulatory compliance, and as sponsor banks, providing the necessary infrastructure and underlying account services for nonbank FinTechs.

FinTechs, in turn, challenge traditional models with technology and development, offering specialized services like advanced fraud prevention, data analytics, and solutions for underserved markets. Their collaboration leverages banks’ established infrastructure, regulatory expertise, customer base and trust with FinTechs’ technological innovation and enhanced user experience, leading to integrated services, new account types like virtual bank accounts and digital wallets, enhanced features, and broader market reach.

Despite the innovation, the report highlights challenges, including navigating complex and evolving regulatory compliance across jurisdictions, mitigating security and fraud risks, ensuring interoperability among diverse platforms and rails, balancing a frictionless user experience with robust security, safeguarding sensitive data privacy, upgrading potentially strained legacy infrastructure, and differentiating in a competitive market.

Looking ahead, the ecosystem’s future promises further innovation, driven by the adoption of real-time payments, advancements in regulatory technology, greater integration of artificial intelligence and machine learning, the expansion of embedded finance into nonfinancial platforms, the growth of decentralized finance, enhanced cross-border capabilities, and a continued focus on financial inclusion.

The benefits of a well-functioning money mobility ecosystem, such as efficient cash flow management, international expansion, cost optimization, and enhanced customer satisfaction, underscore its importance for businesses navigating the financial landscape.