Access to credit, the value of credit in managing personal finances, and fear of debt are all coming into play at a time when over 60% of U.S. households live paycheck to paycheck, including those bringing in six-figure salaries, with many struggling to make ends meet.

These effects are felt most keenly by younger consumers, particularly Generation Z, the oldest of whom are in the early innings of their adult work lives and have yet to establish the bona fides to have access to revolving credit lines or lower-interest cards with sizeable credit balances.

As found in the new study “The Credit Economy: How Younger Consumers Make Credit Decisions,” a PYMNTS and i2c collaboration based on a survey of nearly 3,400 U.S. consumers, 83% made payments for credit products in the last 90 days. And while the data shows that millennial and Gen Z consumers are driving forces for change, using a mix of credit cards and installment loans like buy now, pay later (BNPL), and ushering in a new era of credit use.

According to the report, credit product use closely relates to the number of credit sources available to a consumer, and consumers’ access to credit sources increases with age, as 41% of baby boomers and seniors have three or more credit cards, while among Gen Z, 35% have only one credit card, and 34% have no credit cards with revolving lines.

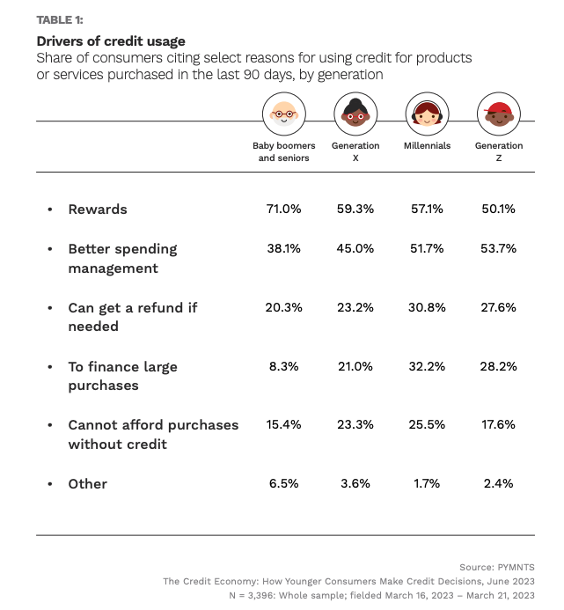

Those with little access to credit are unmoved by rewards points and the like, prioritizing access, which is in stark contrast to Gen X, baby boomers, seniors and even millennials who prize rewards earned through credit card usage, as well as the spend management aspects of credit products. Spend management is one of the few areas where demographics overlap.

Per the study, “Being able to earn rewards may not be the most important reason for Gen Z consumers to use credit products, as the ability to better manage their spending and cash flow is most cited by these consumers. They were most likely to report that better spending management was one of their reasons for using credit for products or services purchased in the last 90 days, at 54%. Millennials were second, at 52%, and 45% of Gen X consumers and 38% of baby boomers and seniors cited the same.”

Given the dominance of credit cards, some may question the value of BNPL, but that would be a mistake. Though a much smaller share of the credit spectrum, BNPL is an accessible form of credit for those with trouble getting cards, as well as for those who can but use the product for the ability to make larger purchases easier to afford via a series of interest-free payments.

While the data shows that five times more consumers used credit cards than BNPL to make a purchase in the last 90 days, the study states that merchants should take note as “The average BNPL purchase was nearly 70% higher than the average credit card purchase, suggesting consumers tend to use BNPL for higher-ticket purchases. In the last 90 days, consumers spent $1,692, on average, via BNPL and $1,006 via credit card.”

With that kind of impact on buying, BNPL is clearly a winner for shoppers, stores and sites.

Among the most revealing findings in “The Credit Economy: How Younger Consumers Make Credit Decisions” are differences in how demographic groups use credit products. As the study states, “Generations’ different financial challenges lead them to make different choices in credit products. Earning rewards drives established and more financially secure consumers to use multiple credit cards, while BNPL has found growing adoption among millennial and Gen Z consumers because of its improved access to funds to manage cash flows along with better terms, often including flexible payment plans outside the traditional 30-day schedule.”

The rise of BNPL is a positive development for retailers and BNPL providers who will need to innovate as the demographics of credit usage change drastically in the coming years.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More